CFC Video Library

CFC Cyber Insurance

CFC offers market-leading cyber insurance that provides comprehensive protection for businesses from the moment coverage begins. Their reactive and proactive approach combines proactive cybersecurity measures with award-winning insurance coverage and unparalleled incident response capabilities. This holistic strategy ensures that organizations are financially protected in the event of a cyber incident and benefit from active measures to prevent and mitigate potential threats, empowering them to stay in control of their digital security.

As a pioneer in emerging risk insurance, CFC leverages advanced technology to enhance its cyber insurance offerings. Their innovative approach utilizes data science and automation to streamline processes and deliver efficient, tailored cyber insurance solutions. This allows CFC to address the rapidly evolving landscape of digital risks faced by businesses across various industries, providing cutting-edge protection in an increasingly complex digital world.

Digital Healthcare

CFC discusses the impact of technology on healthcare and the emerging field of digital healthcare insurance. It highlights how technology improves healthcare by reducing clinician burnout and increasing access to specialized care globally. The video outlines the three pillars of digital healthcare insurance: bodily injury, technology errors and omissions, and cyber events. It also touches on current trends in digital healthcare, including augmented reality, virtual reality, and artificial intelligence. The speakers emphasize the potential of AI in healthcare while noting the importance of its appropriate and unbiased use.

Fintech Companies

CFC features a conversation between Josh and Steve, who discuss fintech companies and their insurance needs. They define fintech companies as financial institutions using technology to deliver services in non-traditional ways, contrasting them with traditional banks with physical presence. The speakers emphasize the importance of regional regulations for fintech businesses and the need for bespoke insurance products due to their unique risk exposures. These exposures include regulatory risks, professional liability, theft, tech failures, and cyber events. The video highlights various types of fintech businesses, such as online banks, payment services firms, and investment companies.

Intellectual Property

CFC features Christian Colesaka and Oliver Hall discussing intellectual property (IP) insurance. They explain that IP insurance covers legal disputes related to intellectual property, including issues of usage, ownership, and validity. The coverage is not limited to companies with IP but can benefit businesses of any size or sector. Premiums for micro-businesses start from a few hundred dollars. The video highlights the value of IP insurance in providing expertise and financial support during disputes, especially for small businesses that may lack experience in this area. They also touch on topics such as patent trolls, the limitations of IP coverage in other policies, and CFC’s broad appetite for IP insurance, with a particular focus on software, manufacturing, and renewable energy sectors.

Life Science

CFC features Paige Davidson, who discusses various aspects of life science companies and their associated risks. She explains that life science companies are involved in the research, development, manufacturing, and commercialization of products designed to identify, treat, or cure diseases and enhance personal health. Paige highlights some unusual risks in the field, such as fecal matter transplants and toilet-based health monitoring technologies. She also mentions the increasing exposure to cyber attacks for life science companies, particularly concerning patient data from clinical trials. Finally, Paige outlines CFC’s appetite for life science insurance, which includes coverage for clinical research organizations, contract manufacturing organizations, and various medical devices.

Management Liability

CFC discusses management liability insurance, explaining its importance for companies of all sizes. The speakers highlight that directors and officers face risks in their day-to-day management decisions, potentially putting their personal assets at stake. The video explains the difference between Side A and Side B coverage in management liability policies, with Side A protecting directors when the company cannot indemnify them and Side B reimbursing the company when it does indemnify its directors. The speakers emphasize that even small and family-run businesses need this insurance, especially given the current economic climate and rising insolvency concerns.

Media Insurance

CFC features Sam Clark and Tom Sketch discussing media insurance, mainly focusing on new media and influencers. They explain that modern media extends beyond traditional publishers and broadcasters to include influencers, podcasts, bloggers, and streaming platforms. The conversation covers how influencers make money through brand deals, sponsorships, and merchandise sales. They also discuss influencers’ primary exposures, such as contract breaches and copyright issues. The video emphasizes the importance of cyber coverage for influencers, as their entire business relies on online content and social media access.

Miscellaneous Professional Liability

CFC features Ellen Ella and Ed Cole discussing Miscellaneous Professional Liability (MPL) insurance. They explain that MPL is a broad category covering professions that don’t fit into specialty teams, with its meaning varying across markets. Critical trends in MPL include the rise of hybrid accounts requiring bespoke coverage, particularly for traditional professional services firms now relying heavily on technology. The speakers highlight CFC’s appetite for various professions within MPL and mention some unusual risks they’ve encountered, including arranging for ashes to be sent to space and lightsaber training.

Non-Fungible Tokens (NTSs)

CFC features Amy Herridge and Mark Weaver discussing Non-Fungible Tokens (NFTs). They explain that NFTs are unique digital tokens containing metadata that authenticate ownership of digital assets, primarily created to establish provenance in the digital art world. The video covers various aspects of NFTs, including their origin in 2014, their rise in popularity since 2017, and the complexities of their ownership rights. The speakers also touch on how NFTs are sold through online marketplaces, the potential for future regulation in the industry, and the distinction between NFTs and cryptocurrencies.

Product Recall Insurance

CFC discusses product recall insurance. They cover various aspects, including what happens during a recall, associated costs, industries most affected, and the link between recalls and reputational damage. The speakers explain that product recall insurance differs from product liability insurance, as it’s a first-party policy protecting the insured’s balance sheet. They also touch on scenarios involving third-party responsibility and mention some unusual risks they’ve encountered, such as a large-scale lobster recall.

Transaction Liability Insurance

CFC discusses transaction liability insurance, particularly focusing on CFC’s seller protect product. The speakers explain that transaction liability insurance helps mitigate risks in mergers and acquisitions. They define key terms like representations, warranties, and indemnities and emphasize the importance of this insurance for all parties involved in M&A transactions, including small businesses and founders looking to sell. The video highlights the advantages of CFC’s seller protect product, including its streamlined process and quick turnaround times.

Stay Ahead in the Cyber Security Game

Learn More about CFC Coverage & Pricing

No Spam. Promise!

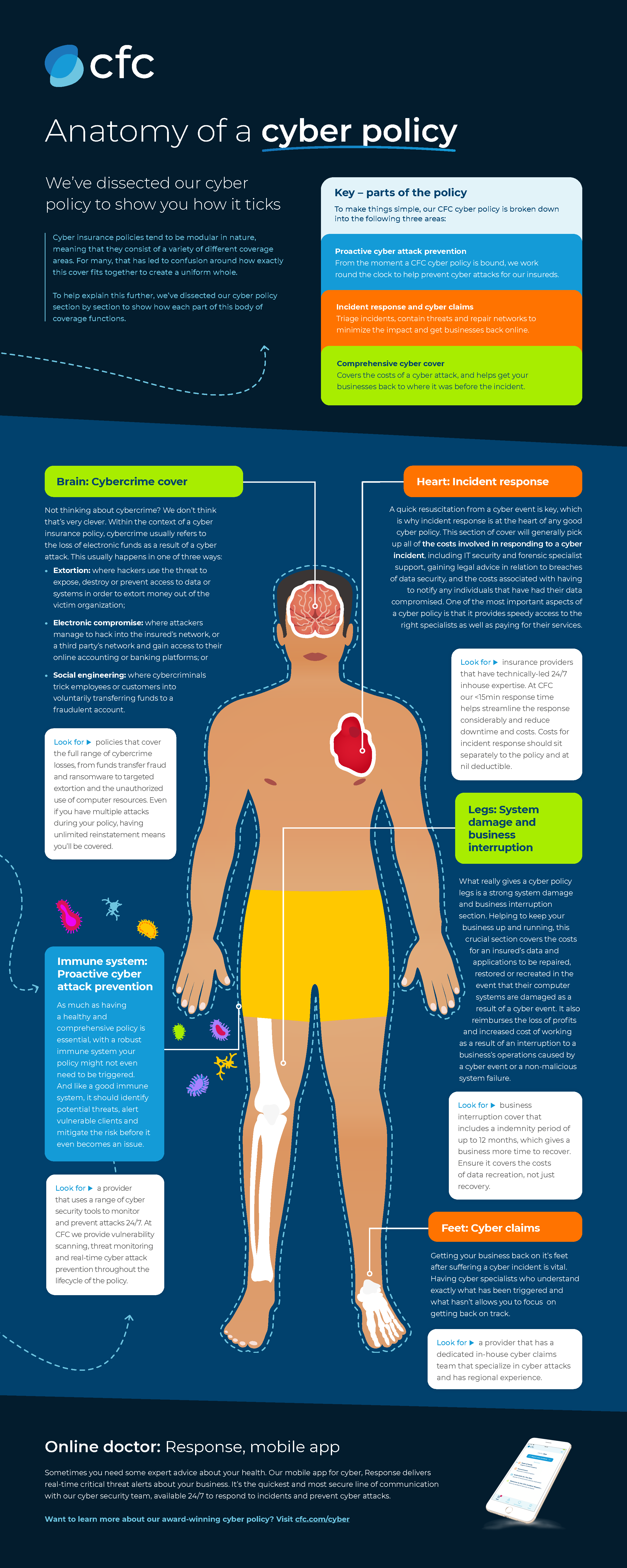

CFC Infographic | Anatomy of a Cyber Policy

CFC Infographic | Six Things Cyber Underwriters Love

CFC Cyber: Infographic – Six Things Cyber Underwriters Love

CFC Infographic | Protecting Your Passwords

CFC Cyber: Infographic – Protecting your Passwords

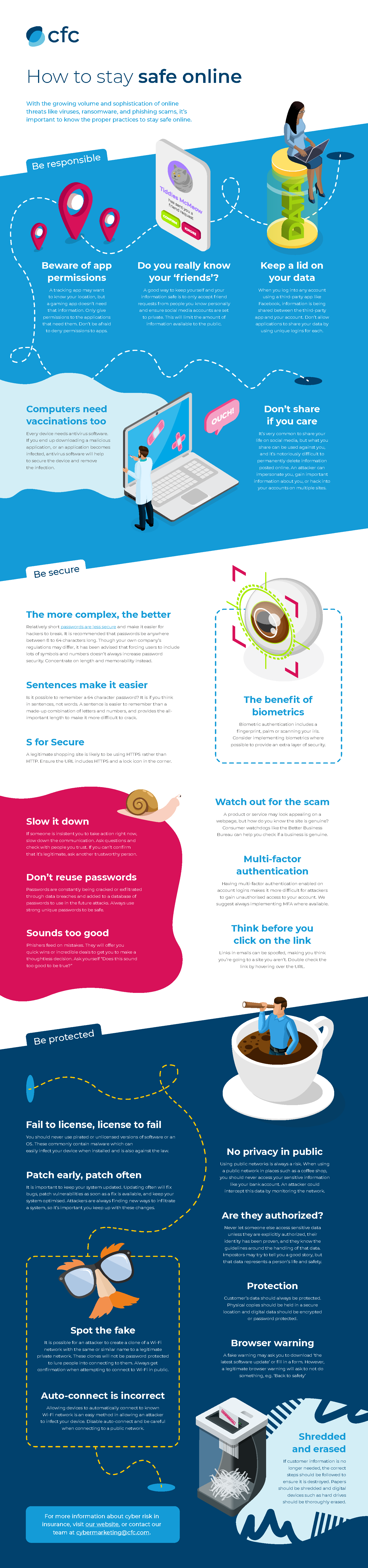

CFC Infographic | Staying Safe Online

CFC Cyber: Infographic – Staying Safe Online

What is Cyber Insurance

Cyber insurance is a specialized insurance product designed to protect businesses against the financial losses and disruptions that can arise from cyber-related incidents, such as data breaches, ransomware attacks, and other cyber threats. This type of insurance typically covers costs related to data recovery, legal fees, notification of affected parties, regulatory fines, and business interruption losses. Businesses need cyber insurance to mitigate the financial impact of cyber-attacks, ensuring they can quickly recover and continue operations while minimizing the potential damage to their reputation and customer trust.

What does cyber insurance cover?

Cyber insurance typically covers costs related to data breaches, including data recovery, legal fees, notification of affected parties, and regulatory fines. It may also cover business interruption losses and expenses related to restoring business operations.

Why is cyber insurance important for SMBs?

Small businesses, often with potentially weaker security measures, are prime targets for cyber attacks. Cyber insurance is a crucial tool in managing the financial burden of such attacks, ensuring they can recover quickly and sustain minimal operational disruption.

How is the cost of cyber insurance determined?

Factors such as the size of the business, the industry, the amount and type of data handled, and the company’s existing cybersecurity measures influence the cost of cyber insurance. Higher-risk businesses or those with poor security practices may face higher premiums.

What are the exclusions in a cyber insurance policy?

Standard exclusions in cyber insurance policies include claims related to pre-existing breaches, acts of war or terrorism, and the failure to maintain minimum security standards. It’s essential for businesses to review policy details to understand specific exclusions and limitations.